I was in the gym the other day and overheard a guy telling another that you shouldn’t be paying $110 a month in car insurance. He told him that you should only have liability insurance because the rest is just fluff. This is the type of thinking that can leave you without a way to recover money for your injuries suffered in a car accident. I told him what insurance he should have in why. This is a breakdown of what insurance you should have and what you could skip on.

What insurance should you absolutely have?

You should have UIM coverage at the very least with liability coverage. As a Seattle personal injury lawyer, I have been heartbroken to see the times where a person is severely injured and comes into my office with no insurance and no insurance on the other guy. If there is no insurance on either side, you have no realistic chance to recover any money in the case. This is because the person who caused the car accident without insurance probably doesn’t have any money to pay for your injuries. Additionally, it’s not likely that a Seattle personal injury lawyer will take your case because there is no realistic hope of ever recovering any money without insurance.

Some studies have show that nearly 30% of drivers are driving without insurance on the road and another 25% have the bare minimum of insurance coverage $25,000. This is why everyone should have UIM insurance. UIM insurance steps in and covers your personal injury damages if you are hit by someone that doesn’t have car insurance or doesn’t have enough car insurance to cover your injuries suffered in a car accident injury case.

PIP insurance is often skipped by people because they believe their medical insurance will cover their medical costs in a car accident. Most medical insurance does not cover chiropractic care and most people have high deductibles that make it so insurance pays very little for their car accident injury treatment. PIP covers all medical costs no questions asked up to your policy amount. Most people choose the $10,000 option but I recommend the higher amount of $20,000. This is because a hospital visit could take up almost all of your $10,000 in PIP leaving you with not much to cover any other treatment you will need like chiropractic, massage, physical therapy, and other doctors appointments.

What insurance could you skip on?

What insurance could you skip on?

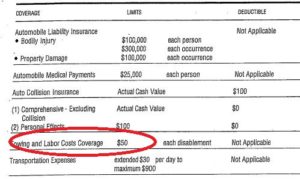

If your car is not worth much, the one insurance policy you could skip is collision coverage. Collision coverage covers the repair and replacement value of your car if you cause a car accident. This is one of the most expensive insurance policies on your policy and may not make sense to have if you have an older car that the cost to repair would be less than your deductible or not much more than it. If your cars value is less than $5,000, it may not make sense to pay extra for collision coverage.

The same goes with comprehensive collision coverage. This covers you in case your car is damages by road debris, rocks, or anything else not caused by a car accident or collision. This is expensive and can usually be avoided. Check your policy on the price.

If you have been injured in a Seattle car accident injury case, you need a Seattle personal injury lawyer. Contact us today for a free consultation on your car accident injury case today.